The finance industry in Guernsey began over 50 years ago, developing from humble beginnings to become the major international offshore finance centre it is today.

Guernsey’s funds industry

Guernsey is one of the world’s largest offshore finance centres, with a thriving funds industry. As of June 2023, over 1,100 investment funds and sub-funds were domiciled in the island with a total net asset value of over US$ 420 billion. When funds not domiciled in Guernsey but under management and administration there are included, this brings the totals to over 1,500 investment funds and sub-funds with a total net asset value of over US$ 515 billion.

This has developed over the last 50 years due in large part to the benefits of long term political and legal stability, combined with tax neutrality, which Guernsey offers. The breadth and depth of fund expertise, supportive regulatory and legal regime, and global market access, combined with its geographic and time zone benefits help to make Guernsey a leading funds domicile[1].

Guernsey is able to provide fund managers and promoters global access. Guernsey is also well placed to benefit from pan-EU passporting rights once granted to non-EU managers under the Alternative Investment Fund Managers Directive.

Regulation of funds in Guernsey

Guernsey operates an efficient simple and flexible regulatory regime.

Every “collective investment scheme” (a “fund”) domiciled in Guernsey will be subject to the provisions of Guernsey’s principal funds legislation - The Protection of Investors (Bailiwick of Guernsey) Law, 2020 (the “POI Law”) - and regulated by Guernsey’s regulatory body for the finance sector - the Guernsey Financial Services Commission (the “GFSC”).

Broadly speaking:

- Every fund domiciled in Guernsey (a “Guernsey fund”) must be administered by a Guernsey company which holds an appropriate licence under the POI Law to do so[2]. The administrator is responsible for ensuring the fund is managed and administered correctly.

- Every open-ended Guernsey fund must also appoint a Guernsey company which holds an appropriate licence under the POI Law to act as custodian (or trustee where the Guernsey fund is a trust). The trustee/ custodian is (with limited exceptions) responsible for safeguarding the assets of the fund and, in some of the rules, to oversee the management and administration of the fund by the administrator.

What constitutes a fund?

Guernsey funds regulation only applies to “collective investment schemes”: arrangements relating to property of any description which have each of the following characteristics:

- the pooling of contributions by investors;

- third party management of the assets; and

- a spread of risk.

Thus arrangements with a single investor or a single asset would not usually be classified as a fund.

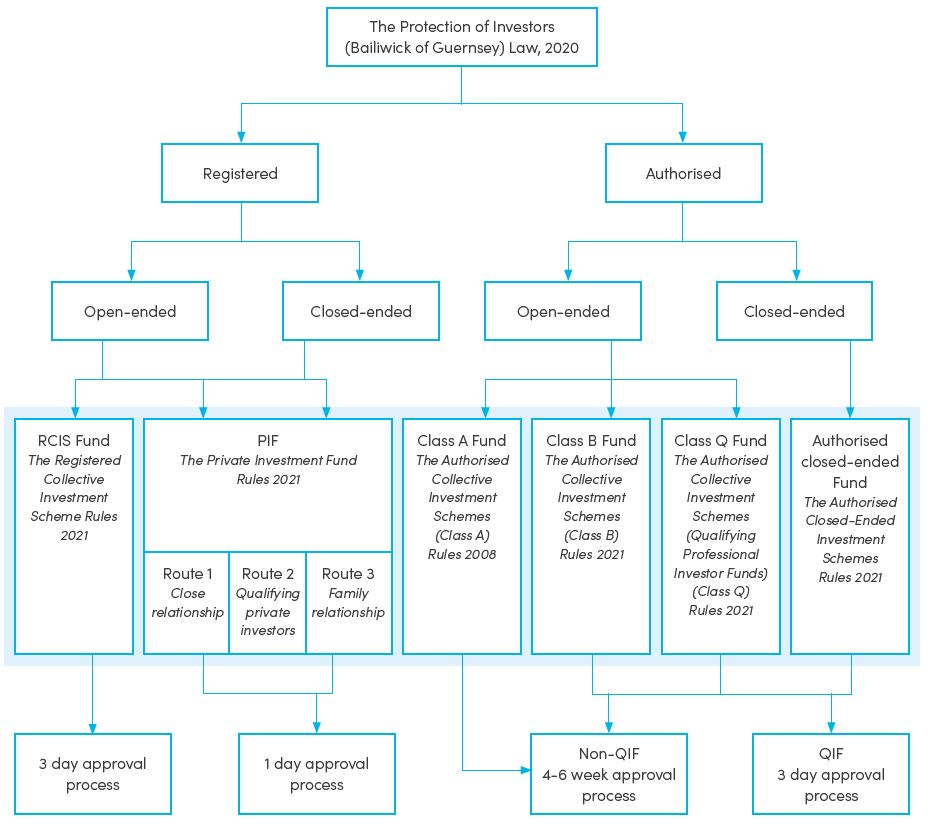

Authorised vs. Registered funds

Guernsey funds are broadly split into two categories:

- “registered funds”, which are registered with the GFSC; and

- “authorised funds”, which are authorised by the GFSC.

The difference between authorised funds and registered funds is essentially that authorised funds receive their authorisation following a substantive review of their suitability by the GFSC, whereas registered funds receive their registration following a representation of suitability from a Guernsey body holding a POI Law licence (the administrator, who scrutinises the fund and its promoter in lieu of the GFSC and takes on the ongoing responsibility for monitoring the fund).

The POI Law grants the GFSC the ability to develop different classes of authorised and registered funds and determines the rules applicable to such classes.

Funds seeking authorisation or registration must therefore satisfy the requirements of the POI Law and (where applicable) the applicable rules specified by the GFSC.

Open-ended vs. closed-ended

The rules governing the different classes of Guernsey funds state whether they are open-ended or closed-ended (or can choose from either).

A Guernsey fund is open-ended if the investors are entitled to have their units redeemed or repurchased by the fund at a price related to the value of the property to which they relate (i.e. the NAV).

There is no prescribed frequency of redemption or period within which the redemption moneys be paid.

Flow chart of Guernsey funds

[1] For a more comprehensive statistical breakdown of the Guernsey funds industry, please see the GFSC’s statistics here.

[2] This is defined in the POI Law as a “designated administrator” in the rules governing the various classes of funds in Guernsey. For simplicity, we have used the term “administrator” to refer to the designated administrator.

Matt is a partner in the corporate team in Carey Olsen’s London office. He advises on corporate and investment funds matters, with particular experience in the structuring and launch of investment funds. Matt provides funds, fund service providers and fund promoters with advice on all aspects of the establishment, regulation and operation of investment funds.

Matt trained at Clifford Chance in London and New York, qualifying as an English solicitor in the Private Funds Group in 2004. While at Clifford Chance he specialised in the establishment of institutional closed-ended investment funds, particularly private equity and hedge funds.

In 2005 he was seconded to ABN AMRO’s investment bank legal department where he advised the fund derivatives desk on the structuring and launch of a broad range of both bespoke and multi-investor institutional fund-linked products.

He joined ABN AMRO in 2007 in a front office capacity, structuring the same products. Following the takeover by RBS, Matt also advised on structured funds, including bespoke, pay-off driven UCITS funds as well as Exchange Traded Funds.

Matt joined Carey Olsen in May 2016.